USF doing the right thing with student loans

In 2016, USF was found to have the lowest rate of defaulted loans among universities and colleges in Tampa Bay, according to a study from the financial products comparison company LendEDU.

Defaulting on student loans occurs when alumni violate the agreed upon repayment plan. For most federal student loans, this occurs when a loan payment is late for more than 270 days.

The statistic is an excellent indicator for USF student success and is much better than the average public college default rate in the U.S. as well as for-profit universities. “For-profit” means that the school operates as a corporation and are often beholden to shareholders.

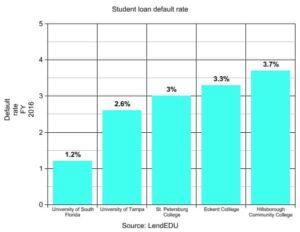

USF was found to have a 1.2 percent student loan default rate, which is No. 239 for lowest rate in the nation and No. 8 for lowest in Florida, according to LendEDU.

The rate is a good indicator of whether a degree received from an educational institution truly helped a student get a job that paid them enough to keep up with their student loan repayments.

The same study found that the national average default rate for the U.S. was 10.1 percent and Florida’s average was 7.33 percent. This means that students at USF are significantly less likely to be in a position where they cannot make their student loan payments.

USF has this ranking because of the affordability of our school without sacrificing the quality of education received.

Specifically, other Tampa Bay universities have higher rates of defaulted loans than USF. University of Tampa has a default rate of 2.6 percent and St. Petersburg College has a default rate of 3 percent, according to LendEDU. However, all of these rates in the area are still much lower than the national average.

At a time of increasing student debt, prospective students need to consider whether there is a high probability of not being able to financially “keep up.” Fifty-two percent of students take out student loans at USF compared to the national average of 69 percent, according to University Scholarships and Financial Aid Services.

The average amount of debt taken out by a USF student is $21,565, which is significantly less than the national average of $29,800.

The same study from LendEDU, which uses data from the Department of Education, highlighted some of the themes that contribute to an increased rate of students defaulting on their loans.

For instance, the best indicators of a high default rate was whether an institution was for-profit. The study found that for-profit colleges and universities had an average default rate of 15.2 percent, public colleges and universities had an average default rate of 9.6 percent and nonprofit private schools had a default rate of 6.6 percent.

There are many lists that highlight USF’s achievements, but this study about defaulting loans from LendEDU is a particularly good illustration of USF’s history of leading students debt free.

Jared Sellick is a junior majoring in political science.

More Stories

OPINION: USF coaches need to be more than game-day leaders

In his first year at USF, baseball head coach Mitch Hannahs brought an old-school approach to the program. He stayed off social media and had minimal interactions with fans, except during press conferences and games. And toward the end of the season, Hannahs began to decline interviews with The Oracle — both for himself and […]

OPINION: Why students should visit MOSI’s planetarium near USF Tampa

Tampa has been home to the second-largest digital dome in the country since April. And it’s right across the street from USF Tampa at the Museum of Science and Industry. I visited MOSI this week to see the Saunders Planetarium and Digital Dome Theater, and I was not disappointed. The price for adult general admission […]

OPINION: USF is showing up for mental health despite federal cuts

Struggling with mental health has become a common experience in college. And yet, instead of responding with urgency, the federal government is cutting funding. But as the federal government is investing less in mental health, USF is doing the opposite. Through investing in research, continuing to support new initiatives and a campus-wide focus on mental […]

OPINION: How USF students can march smart: A guide to protesting

At the No Kings demonstration in Tampa on June 14, I saw firsthand how a well-organized protest can elevate voices, spark conversations and push society forward. But while protests are often powerful, they can also be unpredictable. As tensions rise nationwide around social and political issues, more students are joining protests to make their voices […]

OPINION: $10 million says USF gets artificial intelligence right

Artificial Intelligence often conjures up thoughts of ChatGPT or Snapchat’s My AI. But when perceptions of AI are broadened, its powerful applications in academia become clear. USF has a college focused on AI, which is home to a wide range of research and offers courses to promote ethical AI use. This college is a testament […]

OPINION: Florida schools should get rid of the summer enrollment requirement

Who wants to be cooped up at home all summer, hunched over the computer when you could be at the beach with your friends? Not me. But under Florida’s 6.016 Summer Session Enrollment policy, this is how you may find yourself spending the summer. Florida currently requires all students entering the State University System with […]